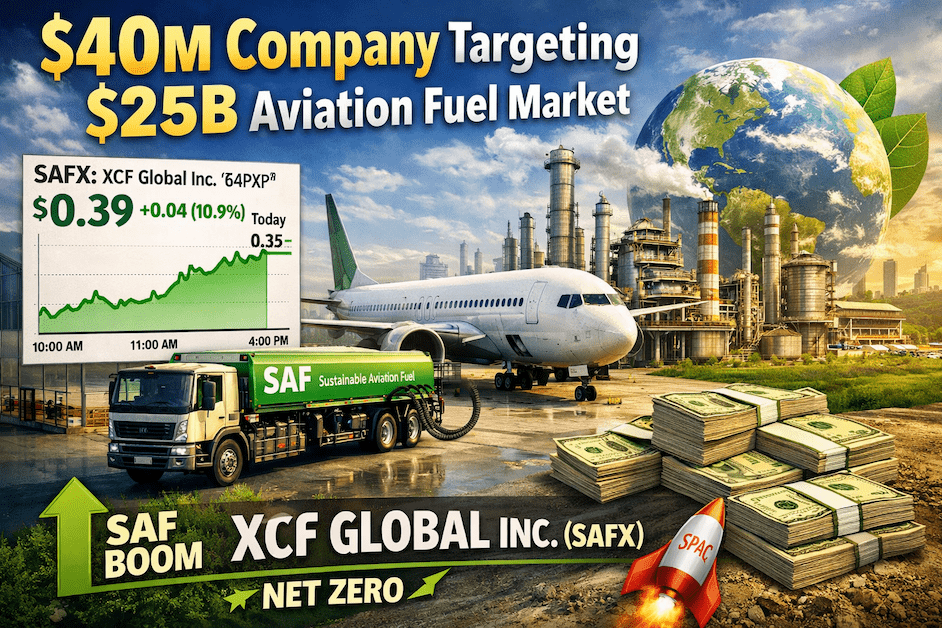

Tiny $40M Company Targeting a $25B Aviation Fuel Market XCF Global Inc. (NASDAQ:SAFX)

SAFX Stock: The Tiny Company Targeting a Massive Aviation Fuel Market as Iran War Risk Reshapes the Energy Trade

XCF Global Inc. (NASDAQ: SAFX) is emerging as one of the only public-market names offering direct exposure to sustainable aviation fuel, and the timing is becoming far more interesting as geopolitical stress pushes traditional fuel markets higher.

On the surface, SAFX looks like a classic speculative microcap: volatile, underfollowed, capital-hungry, and still early in its operating lifecycle. But that simple framing misses the broader strategic setup. SAFX sits at the intersection of three powerful themes: aviation decarbonization, energy security, and rising fuel-price sensitivity. Now, with war-related instability tied to Iran and broader Middle East supply risk sending oil and jet fuel prices sharply higher, that setup becomes more relevant.

Why the Sustainable Aviation Fuel Market Matters

Aviation remains one of the hardest industries to decarbonize. Unlike passenger vehicles, commercial air travel cannot simply pivot to batteries at scale in the near term. That leaves sustainable aviation fuel, or SAF, as one of the only realistic transitional solutions available today.

The investment logic is straightforward. Airlines face mounting pressure to lower emissions. Governments continue to push net-zero mandates and low-carbon fuel incentives. At the same time, traditional jet fuel remains exposed to the same supply shocks, geopolitical risk, and refining bottlenecks that have always haunted the oil market.

That is what makes SAF strategically important. It is not just an ESG story. It is increasingly becoming an energy-security story as well.

What SAFX Actually Does

XCF Global is attempting to build real operating infrastructure in sustainable aviation fuel. This is not a pre-revenue software story wrapped in climate language. The company’s flagship asset is the New Rise Reno facility in Nevada, which is reported to have current production capacity of roughly 38 million gallons per year.

The broader vision is to replicate and scale. Management’s expansion plans point toward a second facility and a larger production footprint that could take annual output toward 80 million gallons. The strategic idea is simple: build, validate, replicate, and scale.

If successful, SAFX is trying to become an early infrastructure layer in the low-carbon aviation fuel market, not merely a promotional ticker attached to a trend.

Why SAFX Trades So Violently

Investors should not romanticize this. SAFX is not a stable compounder. It is a high-risk, high-volatility microcap with a narrative powerful enough to generate extreme price moves.

With the stock recently trading around $0.39, volume surging, and its market value sitting in a small-cap range, SAFX behaves more like a theme-driven trading vehicle than a traditional valuation story. Multi-day spikes of 50% or more are not theoretical here. They are part of the stock’s natural profile.

That volatility comes from three structural features.

1. Microcap Narrative Dynamics

When a company is small, thinly covered, and tied to a hot macro theme, price can disconnect from fundamentals quickly. The lower the float and the stronger the story, the more violent the swings.

2. Capital Dependency

SAFX is still in expansion mode, which means financing matters. Growth is real, but it has to be funded. Shareholder approval for significant new equity issuance and a capital raise tied to plant buildout make one thing clear: dilution risk is not incidental. It is central to the current business model.

3. SPAC Overhang

The company came public through the SPAC route in 2025, which means it carries the familiar pattern many investors now recognize: heavy early hype, sharp de-risking, broad collapse, then a possible second narrative cycle if the operating story stabilizes. SAFX appears to be sitting in that latter stage now.

The Core Bull Case

The bullish argument for SAFX has always been about scarcity and timing.

There are very few publicly traded companies that offer direct exposure to sustainable aviation fuel. That alone matters. If institutions, funds, or retail traders decide they want a public-market vehicle tied to domestic SAF production, SAFX can become a default ticker simply because the universe of alternatives is small.

There is also the policy angle. Clean fuel mandates, subsidies, carbon frameworks, and airline decarbonization goals all work in favor of the SAF theme over time. If the sector matures, the addressable market is large enough that even a tiny company can see outsized percentage appreciation if it secures capital and executes competently.

Then there is platform optionality. The company’s expansion strategy, combined with the potential for partnerships and broader activity across energy and carbon markets, creates the possibility that SAFX evolves into more than a single-facility story. In the best version of the thesis, investors stop valuing it as one plant and start valuing it as an emerging clean-fuel platform.

The Bear Case Investors Cannot Ignore

The bullish setup is real, but so are the weaknesses.

First, this is still a pre-scale business. One primary facility does not make a durable industrial franchise. The company is not yet a proven cash-flow engine, and infrastructure execution is hard.

Second, financing remains existential. If capital markets tighten or enthusiasm fades, the company’s ability to build additional capacity becomes impaired. At that point, the operating dream is subordinate to the balance sheet.

Third, plant development in energy is complex. It is capital-intensive, regulated, and operationally unforgiving. Delays, cost overruns, feedstock issues, regulatory hurdles, or production inefficiencies are enough to break the timeline and pressure the stock.

So the bear case is not abstract. It is that SAFX may be directionally right on the macro theme but unable to fund and execute its way into scale before dilution overwhelms shareholders.

Why the Iran War and Fuel Prices Change the Equation

This is where the story becomes more interesting.

The geopolitical risk tied to Iran and the broader Middle East is not merely another headline. It directly affects the economics of aviation fuel. When conflict threatens oil flows, refining systems, shipping routes, or regional stability, crude prices rise and jet fuel markets tighten even faster. Aviation then feels the pressure immediately because fuel is one of the largest inputs in airline operating cost.

In a normal environment, SAF is often treated as the expensive alternative to traditional jet fuel. But that comparison changes when oil and refined fuel prices surge. The higher conventional jet fuel goes, the narrower the gap becomes between traditional fuel and sustainable aviation fuel.

That matters for two reasons.

1. SAF Becomes More Economically Competitive

When traditional jet fuel spikes, SAF is no longer just a compliance product or a carbon-reduction premium. It starts to look more economically viable relative to the conventional alternative. In other words, higher fossil-fuel volatility improves the relative case for SAF adoption.

2. Domestic Fuel Infrastructure Becomes More Strategic

During geopolitical instability, governments and large industrial buyers stop thinking only about price and start thinking about resilience. They want fuel they can secure domestically, scale regionally, and defend politically. That changes the conversation from “clean fuel” to “strategic fuel supply.”

That shift is important for SAFX. A small domestic producer with physical infrastructure can begin to look more strategically valuable in a world where fuel security matters more than theoretical efficiency.

What the Market May Start Pricing In

If fuel markets remain stressed and policymakers continue emphasizing energy resilience, SAFX could benefit in several ways.

First, the narrative strength improves. The company is no longer just tied to decarbonization; it is tied to supply security and aviation resilience.

Second, the policy backdrop may strengthen. Crises tend to accelerate subsidies, incentives, and strategic funding mechanisms. If governments want more domestic low-carbon fuel production, companies like SAFX become natural beneficiaries in theory.

Third, the scarcity premium can increase. If investors decide they want exposure to this exact pocket of the market, SAFX may attract trading flows simply because there are not many comparable public equities in the same lane.

But there is a counterpoint. Rising energy costs can also pressure the company’s own input economics, logistics, and financing conditions. So the effect is not cleanly positive. It is asymmetric and highly sensitive to execution.

How to Think About SAFX Correctly

The mistake would be to analyze SAFX like a conventional value stock. That is the wrong framework.

SAFX is better understood as a leveraged bet on four variables:

- Strength of the sustainable aviation fuel narrative

- Ability to raise capital and keep building

- Management’s success in executing on infrastructure scale-up

- Geopolitical and fuel-market conditions that make SAF more strategically attractive

That is why the stock can be explosive. If several of those variables turn favorable at once, the equity can reprice quickly. If they move the other way, the downside can be just as severe.

Bottom Line

SAFX is not a simple buy-and-hold story based on present fundamentals. It is a timing-sensitive, narrative-driven, capital-intensive speculation tied to one of the most important long-term shifts in transportation fuel.

The original thesis was already compelling: a tiny public company trying to build a foothold in a potentially massive sustainable aviation fuel market. But the addition of Iran war risk and surging fuel prices adds a more urgent strategic dimension. It means SAFX is no longer only a clean-energy trade. It is increasingly a geopolitical fuel-security trade as well.

The central question for investors is not whether sustainable aviation fuel has a future. It almost certainly does. The real question is whether SAFX can survive financially and execute operationally long enough to scale into that future.

If the answer is yes, the stock has meaningful upside. If the answer is no, dilution and execution failure remain the dominant risks.

That is the setup. SAFX is not being valued on what it is today. It is being judged on whether it can become strategically important before the market stops funding the journey.