Inflation is ‘far from dead’: Why one large asset manager doubts U.S. can hit 2%

A relatively healthy U.S. economy is unlikely to see inflation fall back to 2% “without some amount of pain,” and financial markets are probably pricing in too many rate cuts.

That’s according to James Solloway, chief market strategist and senior portfolio manager at Pennsylvania-based SEI

SEIC,

which oversaw about $1.3 trillion in assets as of September. His views came during a week in which tensions continued to flare in the Middle East and U.S. data pointed to Americans’ willingness to spend despite 5%-plus interest rates and to a labor market that is holding up.

One of Solloway’s biggest takeaways is that wage pressures across major economies are unlikely to subside by enough to be consistent with central banks’ inflation mandates. He is skeptical that U.S. inflation will settle around the Federal Reserve’s 2% target based on a few assumptions, one of which is that oil price declines seen over the past year are not likely be repeated in 2024. Solloway also questions the need for any rate cuts by the Federal Reserve.

“The risks of an escalation in the Middle East are still higher than anybody should feel comfortable with, and actual military conflict could certainly lead to a sharp, short-term rise in oil prices and another supply shock,” Solloway said via phone on Thursday. Such a supply shock “could lead to a ratcheting up of inflation expectations.”

Following the December U.S. consumer-price index reading on Jan. 11 and Thursday’s initial jobless claims data, “there doesn’t seem to be much weakness in the economic numbers looking out for the next six months,” he said. “Inflation between 3% and 4% is a more-than-likely event, and markets are not prepared for that after the last six months of good inflation readings.”

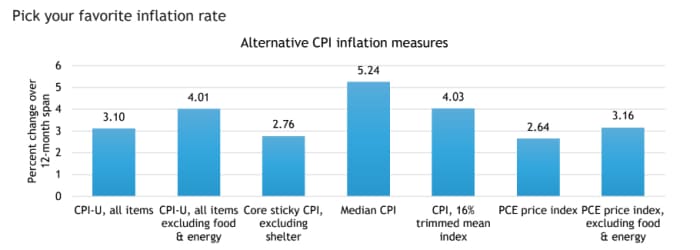

Indeed, core inflation measures, which strip out volatile food and energy prices, for the U.S., U.K., Canada, the eurozone, and Japan suggest that central banks can’t yet declare mission accomplished, according to an 18-page report posted to SEI’s website this month.

Sources: FactSet, SEI. Data as of Dec. 31, 2023.

In Solloway’s view, inflation still has room to run because of underlying cost pressures resulting from higher compensation rates, among other things. In addition, the Israel-Hamas war could escalate, leading to a spike in energy prices, while this year’s presidential election “could be a source of market instability.”

A 3% U.S. inflation rate alone “is not necessarily problematic,” Solloway told MarketWatch. “What is problematic is market expectations, which seem to be pointing toward a return to the environment we had prior to Covid. We’re in a new regime here where inflation tends to be higher and, as a result, interest rates have to stay higher over time.”

Sources: U.S. Bureau of Labor Statistics, Federal Reserve Board of Cleveland, SEI. Data as of Dec. 31, 2023.

See also: Financial markets may be overlooking ‘one remaining ember’ that could reignite inflation

On Thursday, oil futures finished higher after searching for direction as traders assessed the threat to supply from Middle East tensions. Crude, however, has struggled to build in a geopolitical risk premium since the start of the Israel-Hamas war in October, with U.S. benchmark WTI

CL00,

CL.1,

trading around $20 a barrel below its 2023 peak set in late September.

See: Here’s what’s been keeping a lid on oil prices despite risks of a wider war in the Middle East

Earlier in the day, Edoardo Campanella, an international and energy economist for UniCredit Bank in Milan, said he expects Brent prices

BRN00,

BRNH24,

to be pushed into the $80-$85 a barrel range, but sees some risk that those prices could go above $100 if the U.S. steps up sanctions on Iranian oil, the Iran-backed Houthis rebel group starts targeting facilities in Saudi Arabia, or there’s rising instability in the Strait of Hormuz near Iran.

Meanwhile, the lowest level for initial U.S. jobless claims in 16 months pushed 10-

BX:TMUBMUSD10Y

and 30-year Treasury yields

BX:TMUBMUSD30Y

to their highest levels of the new year for a third session. In addition, Treasury’s $18 billion auction of 10-year TIPS drew strong demand from investors Thursday afternoon — indicating a need for inflation protection, according to Tom di Galoma, co-head of global rates trading for BTIG in New York.

Fed-funds futures traders nonetheless continued to cling to expectations for five to seven quarter-point rate cuts from the Fed by December, despite the strength of recent U.S. data. And U.S. stocks

DJIA

SPX

COMP

closed higher, led by a 1.4% rise in the Nasdaq Composite Index.

Changing perceptions about the path of inflation, central banks’ responses, economic growth, and the corporate profit outlook have the potential to upend financial markets, however. Solloway told MarketWatch that a 10% correction in the S&P 500 can’t be ruled out.

In his report, he wrote that “inflation is far from dead, in our opinion.”

“We maintain our position that inflation will not fall all the way back to central banks’ target without some amount of pain,” the strategist wrote. “We think that economies globally will need to endure a prolonged period of subpar growth or outright contraction before labor markets can ease enough to exert enough downward pressure on wages to be consistent with a sustained 2% inflation rate.”